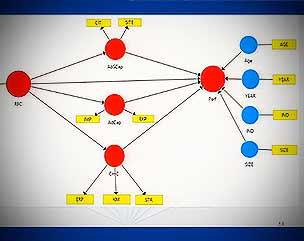

I examine the evolution of contagion indexes between the European financial

sector and the sovereign sector (Austria, Belgium, France, Germany, Italy,

Netherlands and Spain) during the European sovereign credit crisis.

Contagion indexes, Delta CoVaR and Delta CoES, reflect events associated

with extreme left tail returns and interdependencies between defaults

different than those observed in tranquil times. These measures reveal very

useful information concerning risk management. I use a copula approach

with time-varying parameters to capture changes in the tail dependence

between returns in the financial and the sovereign sectors. I employ a

Switching Markov model to identify the most stressful moments of the

contagion indicators. The results point out the emergence of Greek debt

crisis on March 2010 and the vulnerable situation of Spain and Italy in

summer 2011 as the main periods where the contagion from the sovereign to

the financial sector was stronger. The decrease in contagion was gradual

since the speech made by the ECB on July 26th, 2012. The statistical

significance of the change in the contagion indicators is checked using

boostrap tests.

The effect of entry on price. Evidence from the retail gasoline market

Seminarios Ecobas 2017

Valeria Bernardo - Doutoranda en Económicas

Tania Elena González Alvarado - Departamento de Mercadotecnia e Negocios Internacionais

Diversity, Group Size and Performance in Organizations

Brais Álvarez Pereira - EUI and ODI Fellow at the Ministry of Economy and Finances of Guinea-Bissau)

Diversity, Group Size and Performance in Organizations. Questions

Brais Álvarez Pereira - EUI and ODI Fellow at the Ministry of Economy and Finances of Guinea-Bissau)

Xornada informativa a cargo de Manuel Noya, co-fundador e CEO da empresa Linknovate

Manuel Noya - Co-fundador e CEO

O problema do recorte do presuposto en saude en Cataluña

María José Solís Baltodano - Dep. D'Economía

O problema do recorte do presuposto en saude en Cataluña. Quenda de cuestións

Rolda de preguntas

María José Solís Baltodano - Dep. D'Economía

Essays on corporate social responsibility reporting: Enhancing transparency and communication

Nicolás García Torea - Estudante de Ciencias Económicas y Empresariáis

Nicolás García Torea - Estudante de Ciencias Económicas y Empresariáis

Dinámica da especulación nun modelo de burbullas e manías. Quenda de cuestións

Quenda de cuestións

Manuel S. Santos - Economics Department

Anna Bykova - NATIONAL RESEARCH UNIVERSITY HIGHER SCHOOL OF ECONOMICS, PERM

Anna Bykova - NATIONAL RESEARCH UNIVERSITY HIGHER SCHOOL OF ECONOMICS, PERM

Rolda de Preguntas: Que é e que non é a Innovación. Tecnoloxía e Economía

Seminarios da FCCEE

Enrique Mandado -

Risk measures and capital allocations (Question Time)

Emanuela Rosazza Gianin - University of Milano- Bicocca

Contagion spillovers between sovereign and nancial European sector from a CoV aR approach

Javier Ojea - Foundations of Economic Analysis II

Javier Ojea - Foundations of Economic Analysis II